Halifax’s market is finding its balance again. Here’s what that means whether you’re buying, selling or moving up.

6-minute read · By Carlisle Norwood, Broker · May 2026

Halifax’s market has worked its way back to balanced — the most balanced it’s been since before the pandemic. I get the same question from clients, friends, and family every week right now: “is this a good time to buy, sell, or make a move?” Here’s the honest answer.

For most of the last five years, Halifax-Dartmouth real estate has been one of two things: a buying frenzy that punished hesitation, or a slowdown that everyone assumed was the start of something worse. As of April 2026, it is neither. Frenzies are bad for buyers. Crashes are bad for sellers. A balanced market means roughly 4 to 6 months of inventory, where neither buyer nor seller has structural leverage. Combined with strong long-term fundamentals, it’s the first environment in five years that rewards informed decisions on both sides of the table.

Key Takeaways

- HRM has reached the edge of balanced territory (Months of Inventory = 3.9) — the closest it’s been since before the pandemic.

- Buyers now have real negotiating leverage in the premium tier; the $400K–$600K band is still competitive.

- Sellers still win, provided pricing reflects the last 90 days of comps, not 2022 highs.

- The pressure has eased, not disappeared. Federal immigration targets were cut for 2026 — sharply for students and temporary workers — and that’s a big reason demand cooled. But the structural housing shortage is still there, and 2027–28 targets aren’t locked. If policy reverses, demand returns quickly.

What the data shows

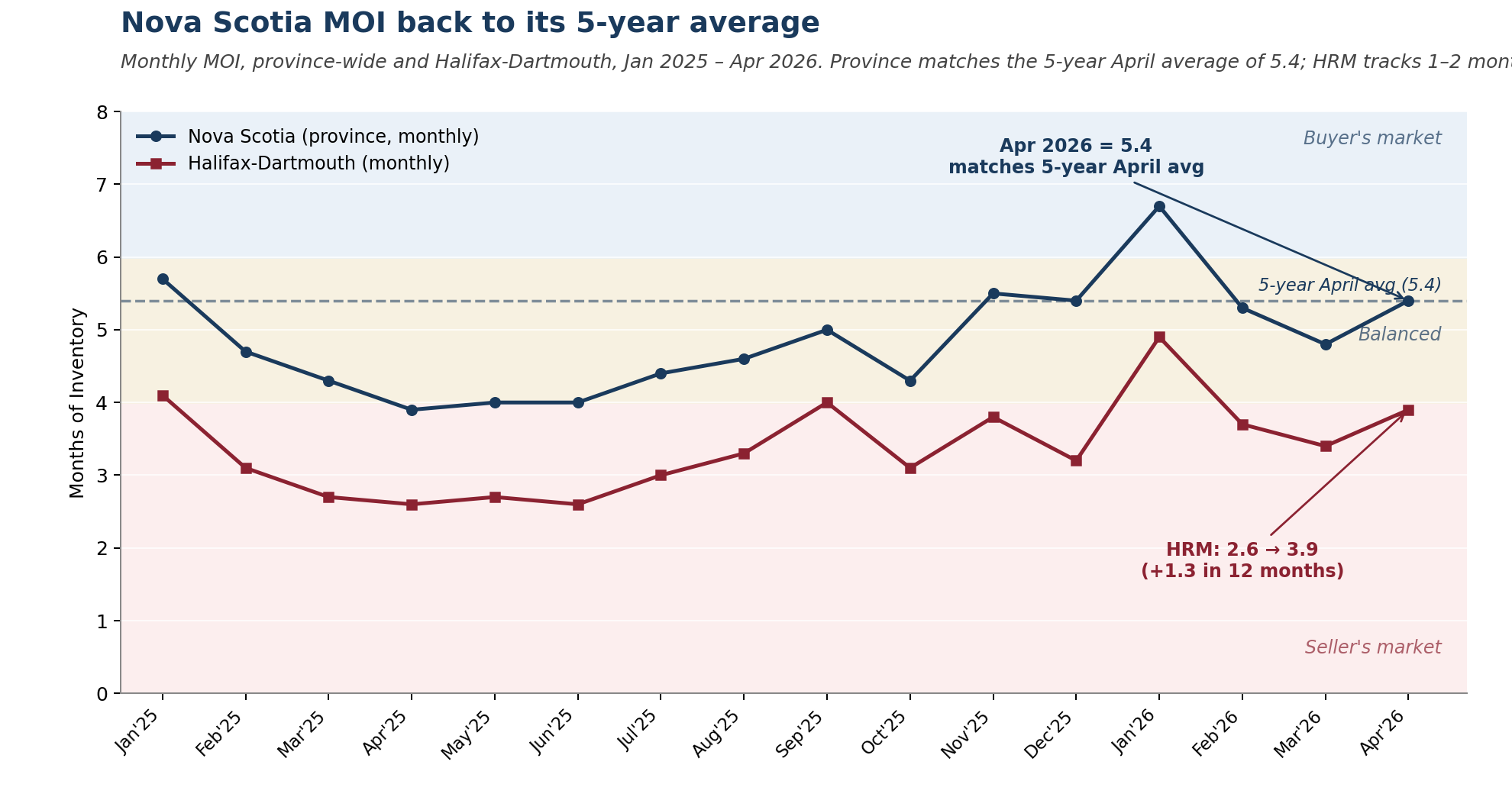

Halifax-Dartmouth went from a seller’s market to a balanced one over the last twelve months. The clearest measure is Months of Inventory, how long it would take to sell every active listing at the current pace. HRM was at 2.2 in April 2024, 2.6 in April 2025, and 3.9 in April 2026. Anything under 4 historically signals seller-leaning conditions; 4 to 6 is balanced. At 3.9, Halifax is right at the line — functionally balanced, and trending into the band rather than away from it. Worth noting: the province crossed into balanced territory earlier and has held there for over a year. HRM is the later mover, now catching up.

Province-wide, the same trajectory is visible monthly, with HRM tracking 1–2 months below the provincial line:

Figure 1 — Monthly Months of Inventory, Jan 2025 – Apr 2026.

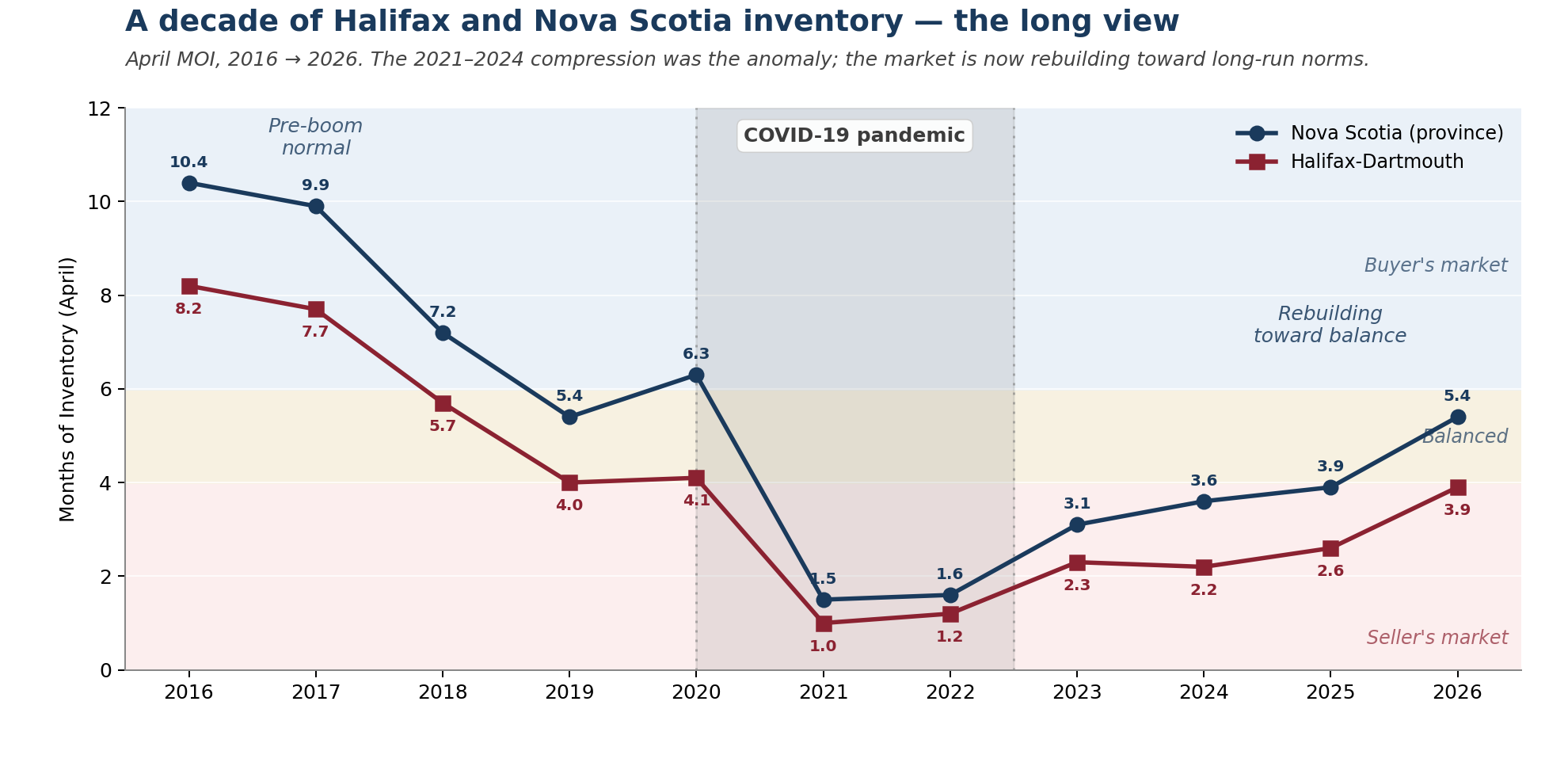

Zoom out and the same story is even clearer. The pandemic-era compression — roughly the 2020 rate collapse through the 2022 rate hikes — was the anomaly, not the baseline:

Figure 2 — Months of Inventory (April only), 2016 → 2026.

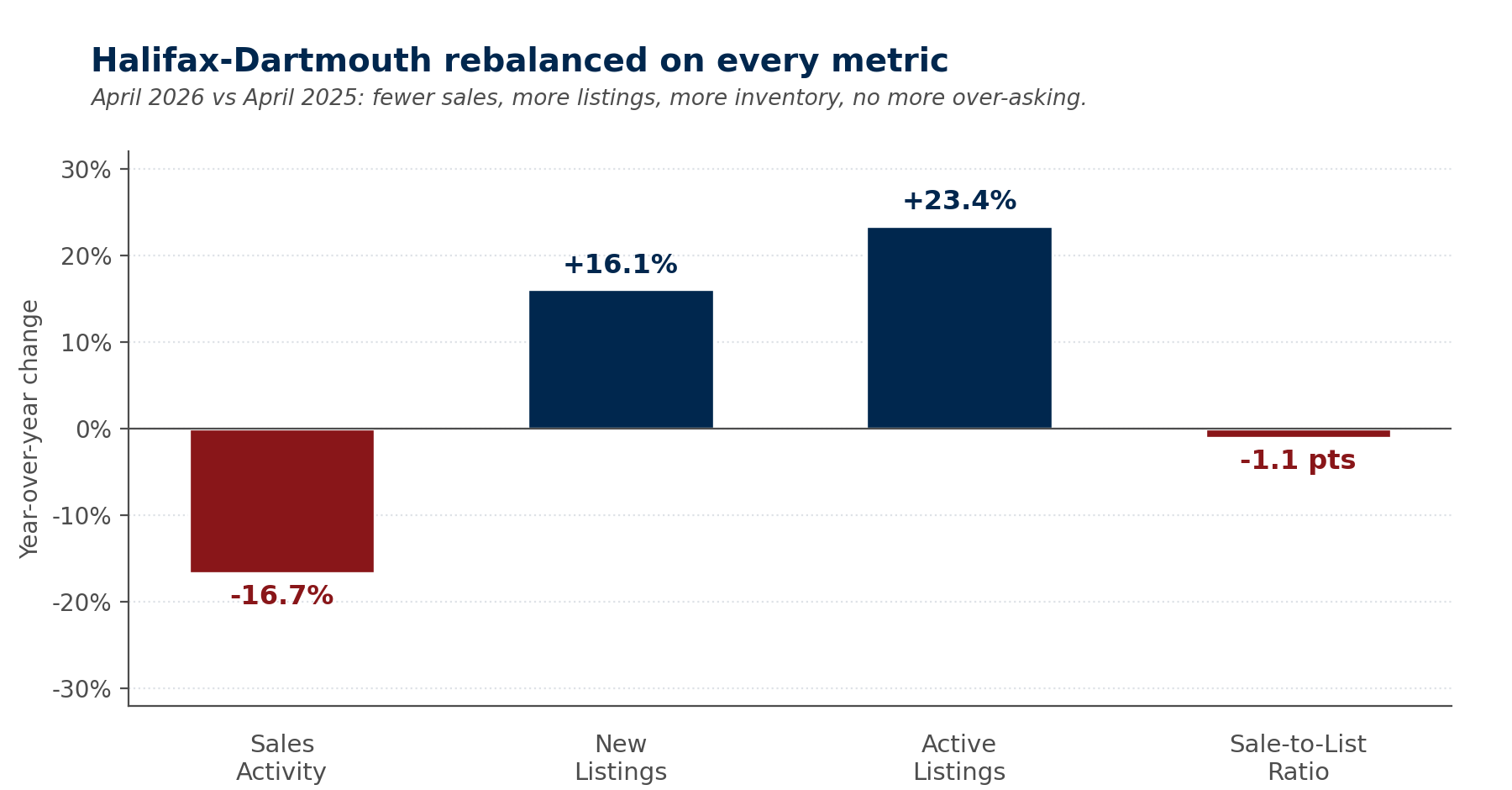

MOI is the headline, but the other HRM metrics moved with it. Five metrics — and not one points back toward a seller’s market. Sales down year-over-year, new listings up, active listings up, days on market essentially flat, sale-to-list ratio below 100.

| Metric (HRM, April YoY) | April 2025 | April 2026 | Direction |

|---|---|---|---|

| Sales activity | 509 | 424 | ▼ Down 16.7% |

| New listings | 778 | 903 | ▲ Up 16.1% |

| Active listings | 1,326 | 1,636 | ▲ Up 23.4% |

| Median days on market | 23 | 22 | ◆ Roughly flat |

| Sale-to-list price ratio | 100.1 | 99.0 | ▼ Below 100 |

Figure 3 — Halifax-Dartmouth year-over-year change, April 2026 vs April 2025.

More inventory. More time on market. No more bidding wars over asking. Prices did not collapse. The HRM Home Price Index (HPI) Composite Benchmark is still positive on a 12-month basis, and Nova Scotia’s province-wide HPI is up 32.3% over five years. What happened isn’t a price reset. It’s a return to normal velocity.

Why the market balanced — and what could tip it again

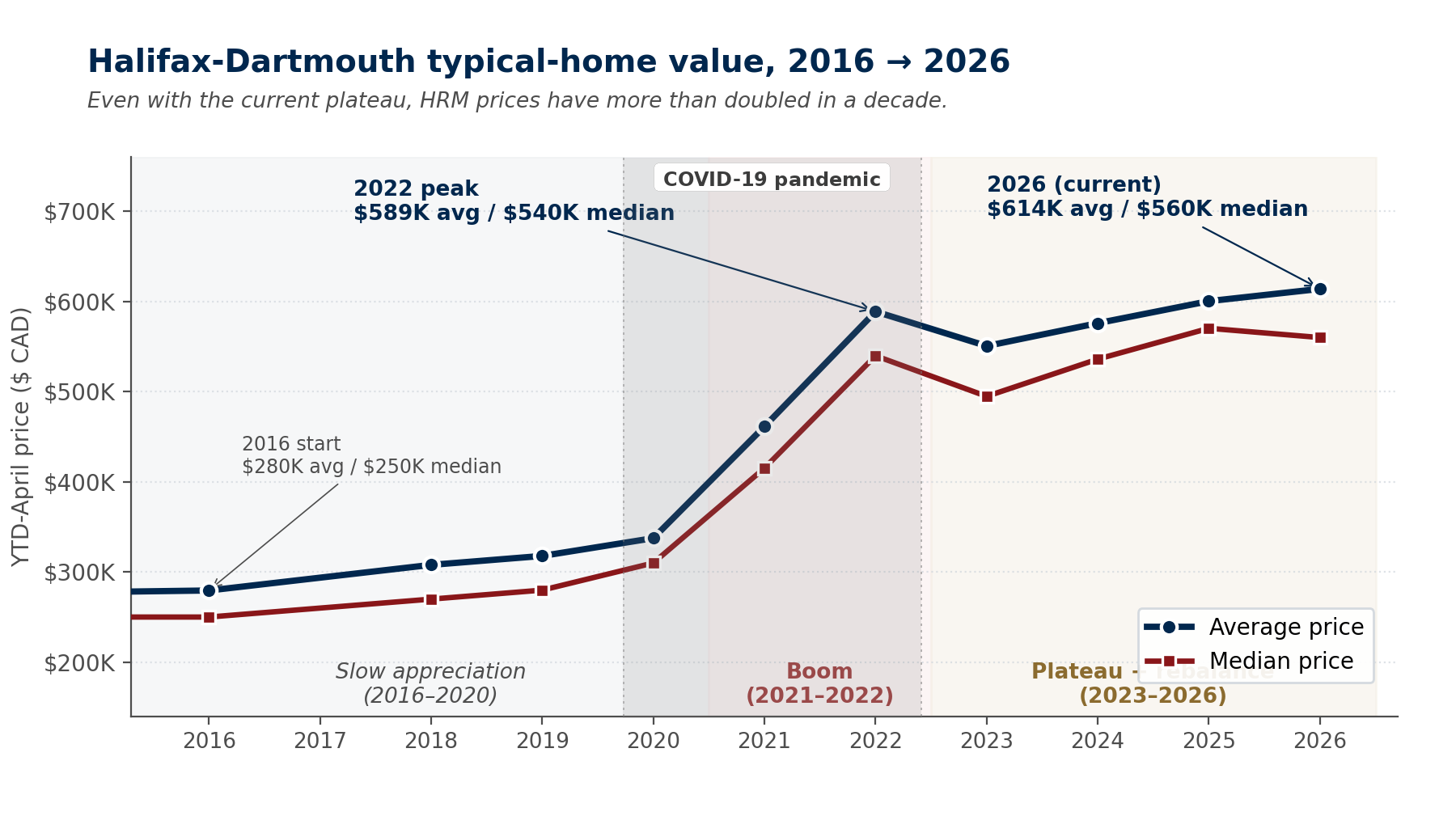

The decade view explains it in one picture. Halifax-Dartmouth values have more than doubled since 2016. The current plateau is the small flat section on the right of the chart, modest in context.

Figure 4 — Halifax-Dartmouth typical-home value, 2016 → 2026.

So how durable is this balance? Here’s my read — and I want to be upfront that this is opinion, not prophecy. Nobody can tell you where interest rates, federal policy, or the global economy land in eighteen months.

But the mechanics aren’t complicated. The last five years of price pressure came from demand outrunning supply. The biggest accelerant on the demand side was population growth — Nova Scotia added more than 100,000 people since 2020. Federal immigration targets have since been cut, sharply on the temporary-resident side, and almost on cue, the market cooled to balanced.

What didn’t change: we still aren’t building anywhere near enough homes to close the gap — for buyers or for renters. So the supply shortage didn’t get solved. The demand that exposes it just got turned down.

Translation: today’s leverage exists because demand paused, not because demand left. That’s why I’d watch three things, not one — immigration policy, interest rates, and the broader economy. If immigration ramps back up, if rates fall far enough to pull buyers off the sidelines, or if the economy stays resilient, demand returns and a 3.9 starts heading back toward 2.6. If the economy weakens instead, balance could hold longer. Supply and demand, simply put — but with more than one lever in play.

For buyers

What this means if you’re buying

You have negotiating leverage you haven’t had since 2020. Active listings in HRM are up 23% year-over-year. The buyer who showed up to seven offers per house in 2022 is showing up to one or two now.

Sale-to-list ratios (the price homes actually sell for as a percentage of asking) are just under 100, which means homes are selling at or slightly under asking, not 5 to 15 percent over. Inspection and financing conditions are normal again. Counter-offers are real conversations.

That leverage is concentrated in specific tiers. Premium HRM (Bedford, Kingswood, Waverley, Halifax Peninsula upper-end) is where the inventory build has been most pronounced; days on market in these neighbourhoods are running 28+ days. If your shortlist was in this range, this is the cleanest negotiating environment since 2018.

Lower Sackville sales were actually up 15.6% YoY against an 18.9% drop in new listings. Fewer homes hitting the market, but more of them moving. If you’re shopping in the $400K–$600K band, you’re still in a competitive market, and the rules are different.

- Get fully pre-approved. Lock in your rate and qualification window.

- Define your real criteria. Balanced markets reward buyers who know what they want and can move when they see it.

- Waiting for a crash? The supply data argues that’s not the bet most evidence supports.

- Use your inspection conditions. They’re back. Use them properly.

For sellers

What this means if you’re selling

The frenzy is over. Properly priced homes still move in three to four weeks. Improperly priced homes sit for 60+ days and eventually sell for less than they would have at correct asking.

Pricing discipline is not pessimism. Halifax-Dartmouth median sale prices are within 1% of where they were a year ago, and your equity from the last five years remains intact. Provincial HPI is up 32.3% on a five-year basis, and HRM has done better. The peak was real, and the peak became your equity. What’s changed is that buyers will no longer reward optimistic pricing on the way to closing. They will reward correct pricing, promptly.

- Price against the last 90 days of local comps. Not 2024. Not what your neighbour got two years ago.

- Presentation matters. A 2026 buyer with options will negotiate hard against a tired home and easy against a clean, well-presented one.

- Don’t fear deliberate buyers. The buyer who takes a week to come back with a measured offer is a more reliable closer than four over-asking offers in a weekend.

If you’re waiting for 2022 to come back, the data says it won’t. But you don’t need it to. A balanced market with intact equity is a perfectly good market to sell in, provided you price and present well.

For move-up clients

What this means if you’re moving up

This is the most strategically interesting position in the current market. A move-up is really two transactions: selling your current home, and buying a bigger one. In hot markets, the bigger home is appreciating faster — so the upgrade keeps getting more expensive the longer you wait. A balanced market is the window where that gap pauses. And once you’ve moved up, every future dollar of appreciation accrues on a larger asset — and stays tax-free as your principal residence.

In a balanced market with strong long-term fundamentals, which is exactly where Halifax sits right now, you transact on both sides at fair value. You sell with realistic pricing discipline, you buy with negotiating leverage, and the spread between sale and purchase closes meaningfully.

- Bridge financing is back on the table in 2026. Lenders are willing to extend a short-term loan that lets you close on the new home before your current one sells. They weren’t, in 2022.

- Sale-of-property conditions are accepted. Your offer on the next home can be contingent on selling your current one. You don’t have to win the buy before you’ve sold.

- Premium-tier negotiating room is at a 5-year high. Bedford, Kingswood, Waverley, and peninsula upper-end (the homes most move-ups want) are all flexible right now.

- The principal-residence advantage scales with you. In Canada, the gain on your primary residence is generally exempt from capital gains tax. Move up, and any future appreciation compounds on a larger asset — and stays outside the CRA’s reach. It shouldn’t drive the decision, but over a long hold it’s a real, quiet tailwind that most move-up clients underweight. (Confirm the specifics with a tax professional.)

If you’ve been waiting for the math on a move-up to work, this is the cleanest window for that math we’ve seen in years.

The bottom line

Halifax has had three kinds of markets in five years: a runaway frenzy, a transition, and now a balanced market with intact long-term fundamentals. The structural conditions that drove the last decade haven’t gone away. They just have less immediate pressure on them. That balance is real, and it’s likely to hold for as long as the current conditions do: immigration restraint, steady-ish rates, a stable economy. If those shift, the math changes. I won’t tell you which way it breaks — but I’ll tell you it’s worth watching.

If any of this matches your situation, the value of a 15-minute conversation right now is higher than it’s been at any point in the last five years.

Email Carlisle: let’s talk through your situation →

We’ll walk through your specific neighbourhood, your price point, and the realistic options open to you right now.

“Working with Carlisle and Sara made the stressful experience of selling a house as pleasant and streamlined as it possibly could have been. Highly recommend reaching out to them for your real estate needs!”

— Evan, recent Halifax seller

About the author

Carlisle Norwood — Broker, Full Circle Realty Inc.

Halifax-based broker, investor, and lifelong Nova Scotian. Carlisle has spent more than a decade helping Maritime families navigate buying, selling, and building investment portfolios across HRM and the South Shore.

Keep reading

→ Prices finished 2025 higher across Halifax, Dartmouth and Nova Scotia — January 2026

→ Market Stabilization Continues: Inventory Rises as Prices Hold Steady — November 2025

→ Halifax and Dartmouth Lead Nova Scotia’s Steady October Market — October 2025

Sources & methodology

All market activity data from the Nova Scotia Association of REALTORS® MLS® Monthly Reports, January 2025 through April 2026, prepared by the Canadian Real Estate Association on behalf of NSAR.

HPI Benchmark Prices are calculated by CREA using a hedonic pricing model that controls for housing type, age, size, and features.

Housing supply gap context from the Canada Mortgage and Housing Corporation (CMHC)’s 2025 update to its Housing Shortages in Canada series.

Population data from Statistics Canada quarterly estimates (Table 17-10-0009-01) and Nova Scotia Department of Finance.

This post is not personalized investment, legal, or tax advice. Any real estate decision should be made in consultation with your own broker, lawyer, and financial advisor.